Featured

Table of Contents

There is no government debt relief program for credit cards. You can, however, discover financial obligation relief for charge card through other opportunities. Financial obligation relief companies provide services to help you handle and settle credit card financial obligation for less than you owe. This is called debt settlement. When you settle credit card financial obligation, you and the credit card company settle on an amount you'll pay, which is less than the total balance you owe.

If you don't have a lump amount to use your financial institutions (the majority of people don't), you might choose to stop making charge card payments and instead reserved money in a devoted account. If you stop paying your lenders for any reason, anticipate credit report damage and collection efforts. When you have actually enough saved to use your lenders, negotiations can start.

Insolvency filings are public records and can make it challenging to get tasks in specific fields. You likewise offer up control when you submit bankruptcythe court tells you how much you will pay (Chapter 13) or what properties you need to provide up (Chapter 7) to satisfy your creditors. Insolvency has a significant negative influence on your credit rating.

On the professional side, debt settlement could help you leave debt quicker than making minimum payments, given that you're paying less than the total balance. A downside of picking debt settlement for debt relief is that it's most likely to damage your credit standing. Keep in mind, however, that if you're currently falling back on your payments, the odds are good you've currently seen an unfavorable effect on your credit report.

If you're considering credit card financial obligation relief programs, research study your options thoroughly. Examine the services offered, the charges, and online evaluations to see what other individuals are stating. Regardless of which financial obligation relief program you select, the most crucial thing is taking action to get your financial resources and credit back on track.

Steps to End Illegal Harassment From Credit Collectors

There may also be some drawbacks. It is very important to understand both the benefits and drawbacks. Customers with federal government trainee loans may receive income-driven payment strategies. These strategies can make a huge distinction. They base your regular monthly payments on a percentage of your income. This assists ensure you can pay for those payments.

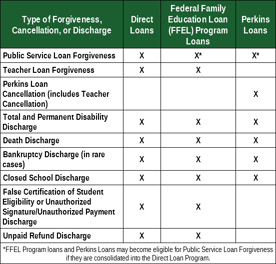

Working long enough in specific public service professions could certify you to have the remainder of your financial obligation forgiven. Might paying into an income-driven repayment program for 20 or 25 years. If you've ended up being totally and permanently handicapped, you may not have to repay your student loans. Check for more details and to discover out if you qualify.

Financial obligation forgiven under federal student loan programs is generally an exception. There are a few states where forgiven federal trainee loan financial obligation might be treated as taxable earnings.

Proven Ways to Negotiate Overdue Debt

Let's attend to some common misconceptions about federal government financial obligation relief programs to clear up any confusion. Reality: Oftentimes, IRS and student loan financial obligation forgiveness programs are based on your ability to pay. So, while they decrease the quantity you owe, they may not entirely remove your debt. Reality: Different programs have various eligibility requirements.

Latest Government Debt Relief Solutions for 2026Reality: The application procedure may take some time. There are numerous resources and assistance systems offered to assist you. Now that we've debunked these myths, you can better understand what government debt relief programs can use.

These programs are developed to help, not to include more stress. It deserves exploring your alternatives. Federal government debt relief programs don't cover all kinds of debt, but there are other options that can help. Personal professionals and challenge programs can offer assistance and options. Here's what you can do if you have financial obligation issues the government can't resolve.

These organizations include personal debt relief business and not-for-profit credit therapists. Here are some of the options they might use: Hardship programs: Lots of creditors provide challenge programs to assist you make it through bumpy rides. These programs may lower or pause payments, lower interest rates, or waive fees for people experiencing financial trouble.

Expert Advice for Resolving Consumer Debt

This might lead to substantial financial obligation reduction. Credit counseling: A certified credit therapist can help you create a budget and find out money management skills if you enroll in their financial obligation management program. If you have debt issues, begin taking steps to fix them: Connect to creditors to inquire about difficulty programsTalk to a financial obligation relief professional or credit counselor for a free consultationConsider which service best fits your situationAct quickly so you do not build up more debt or face collection actionsGovernment financial obligation relief programs might become part of the option for you.

Home debt in America is over 18 trillion dollars, according to the Federal Reserve Bank of St Louis. With so much debt, it's not surprising that lots of Americans desire to be debt-free.

Financial obligation is always a monetary problem. But it has actually become harder for many individuals to manage recently, thanks to rising rate of interest. Rates have increased in the post-COVID age in reaction to unpleasant economic conditions, consisting of a surge in inflation triggered by supply chain interruptions and COVID-19 stimulus costs.

While that benchmark rate does not straight control rates of interest on debt, it affects them by raising or lowering the cost at which banks borrow from each other. Added costs are generally handed down to consumers in the form of higher rates of interest on debt. According to the Federal Reserve Board, for instance, the typical rate of interest on credit cards is 21.16% since Might 2025.

Comparing Professional Debt Settlement Services in 2026

Card rate of interest may likewise increase or remain high into 2026 even if the Federal Reserve alters the benchmark rate, because of growing financial institution concerns about rising defaults. When lenders hesitate customers will not pay, they frequently raise rates. Experian also reports average rates of interest on auto loans hit 11.7% for used vehicles and 6.73% for new cars and trucks in March 2025.

Individual loan rates are also higher. With numerous kinds of financial obligation becoming more pricey, lots of people desire to handle their debt for goodespecially provided the continuous financial unpredictability around tariffs, and with a recession risk looming that could impact work prospects. If you are scared of rates rising or the economy faltering, placing yourself to become debt-free ASAP is among the smartest things you can do.

{kind=link}

Latest Posts

Restoring Your Credit Health After Bankruptcy

Essential Rules for Starting Bankruptcy in 2026

Expert Strategies for Managing Personal Debt